HK: a hub not only for Finance, but Green Finance

Worries about the impact of climate change might not have started out as an urgent action item for financial institutions around the world, but this has changed in recent years, particularly in light of the rising costs of climate-induced damage. As a result, insurers have seen their money lost to natural catastrophes rise sharply over the past three decades. According to data from Swiss RE, insured losses as a result of natural catastrophes topped 90 billion in 2020, the 5th highest on record, while all-time high annual losses of USD 157 billion occurred in 2017. Swiss RE Institute says that only 44% of the economic losses in 2020 stemming from natural catastrophes were insured. However, the average of 44% does not reflect an accurate picture, as reinsurance company Munich RE's data shows that in Asia, only USD 3 billion worth of losses were insured out of total estimated losses of USD 67 billion in 2020.

Hong Kong in particular is subject to a high degree of risk related to natural disasters such as storms, floods and wildfires, according to research by ARCADIS, a design and consultancy organization for natural and built assets. However, insurance ratios appear to be quite high in Hong Kong, creating a greater potential burden for insurers. As an example, the Hong Kong Monetary Authority (HKMA) noted that Super Typhoon Mangkhut that took place in September 2018 wiped USD 400 million worth of assets, of which insured losses amounted to USD 370 million, according to Swiss RE.

Partly as a result of this event, and following what now appears to be a global trend, the Hong Kong government in 2017 released its “Climate Action Plan 2030+”, a multi-dimensional response to increasing threats posed by climate change. Because the SAR plays a critical role within the global financial sector, Hong Kong sees climate change preparedness as an essential part of a larger strategy to position itself as a green finance hub, and activities that will be undertaken for the remainder of 2021 will play a pivotal role in this effort.

Banking: Stress Testing for Climate Risk

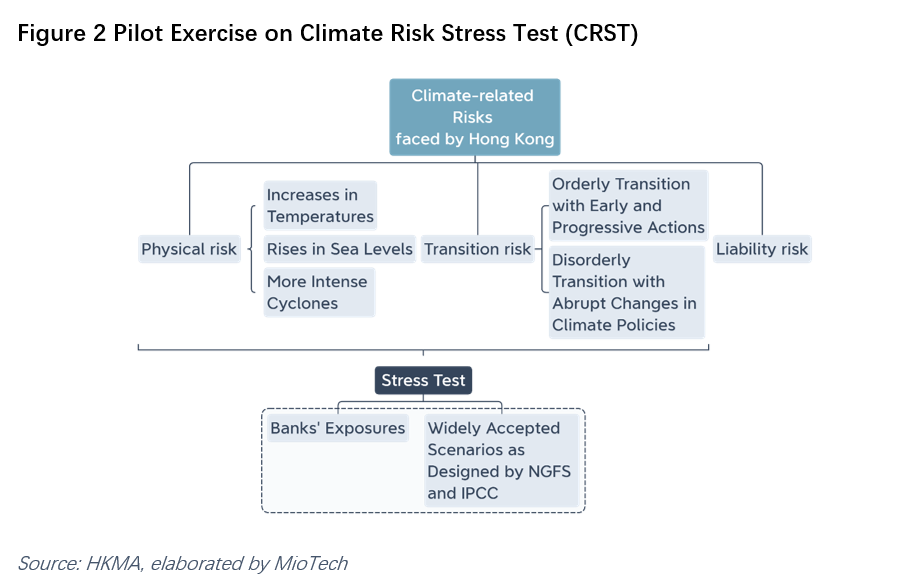

The United Kingdom took the lead in prioritizing climate change in late 2019 when it started to stress-test banks for climate risks. This was followed by Hong Kong in late 2020 and the European Union in early 2021. The Hong Kong government’s push to ensure climate change preparedness was brought to the doorstep of the banking sector in December of 2020, when the HKMA invited banks to take part in a pilot climate risk stress test (CRST) scheduled for 2021. When it was first scheduled, the CRST was voluntary and only open to banks which expressed interest. To carry out the test, the HKMA proposed the use of scenarios such as those adopted by the Network for Greening the Financial System (NGFS) for Central Banks and Supervisors; it also took into consideration the HKSAR banks’ own exposure to different forms of climate change risk.

The planned pilot stress test would cover two types of risk: physical and transition risk. Physical risk is defined as the damage and loss of physical assets, as well as trade and supply chain disruptions in the event of severe climate-induced events, which the HKMA have identified as exposure to temperature increases, intense cyclones and rising sea levels.

Aside from physical risk, the HKMA would also be testing banks for transition risk, which covers two probable transition pathways toward attaining the goal of a low carbon emission economy. These paths are an orderly transition with early and progressive actions and a disorderly transition with abrupt changes in climate policies. Although future policies remain unknown, Hong Kong’s seriousness in tackling the effects of climate change is evident, particularly after chief executive Carrie Lam vowed in her 2020 Policy Address that the city would become carbon neutral by 2050, having hit peak emission in 2014.

Green Finance: Adapting to Global Standards to Boost Hong Kong’s Presence

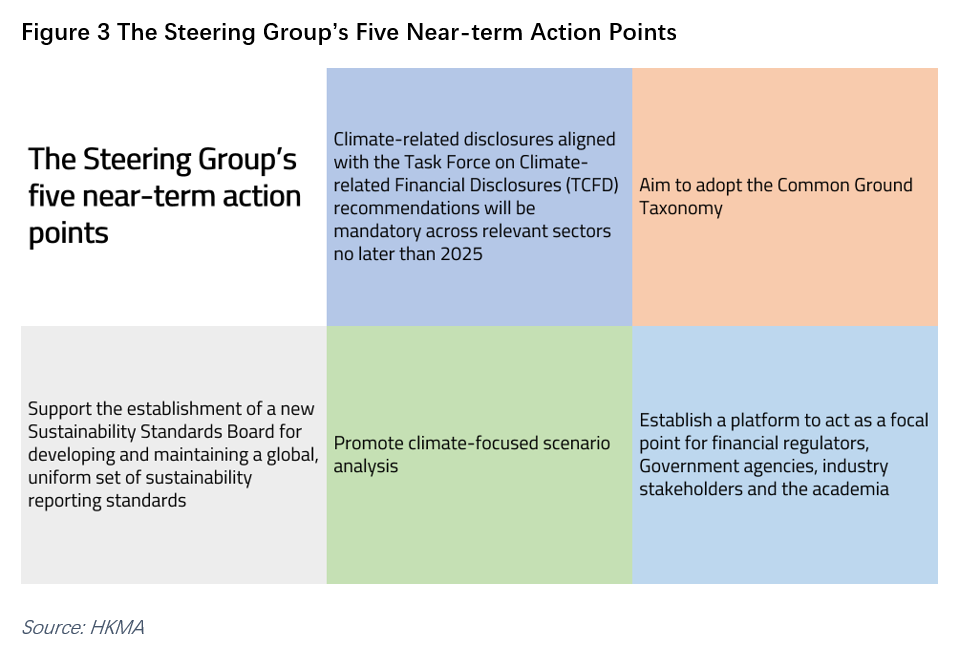

Hong Kong’s climate ambitions are not limited to the banking sector; the S.A.R. has begun to improve and upgrade its financial ecosystem as a whole in order to embrace opportunities brought by a transition to low-carbon economy. In December 2020, the Green and Sustainable Finance Cross-Agency Steering Group announced a strategic plan which contains five near-term actions, namely: requiring mandatory disclosure against Task Force on Climate-related Financial Disclosures (TCFD) by 2025; aiming to adopt the China-EU Common Ground Taxonomy; supporting the developing and maintaining of universal sustainability reporting standards; and promoting climate-focused scenario analysis, establishing a cross-sector collaboration platform.

Of note is the action point calling for climate-related disclosures to be mandatory across relevant sectors by 2025. This goes one step further, particularly in relation to existing requirements on listed companies and financial institutions, and where the disclosures are not mandatory for many aspects of the environmental and social pillar. Hong Kong is the first Asian economy to impose this requirement, said Eddie Yue, Chief Executive of the HKMA.

Hong Kong will further look to adopt the Common Ground Taxonomy when it is developed in mid to late 2021 by the International Platform on Sustainable Finance (IPSF) Working Group on Taxonomies co-led by China and the EU, as two of its financial authorities HKMA and Securities and Futures Commission are members of the IPSF.

Capital Market: the STAGE

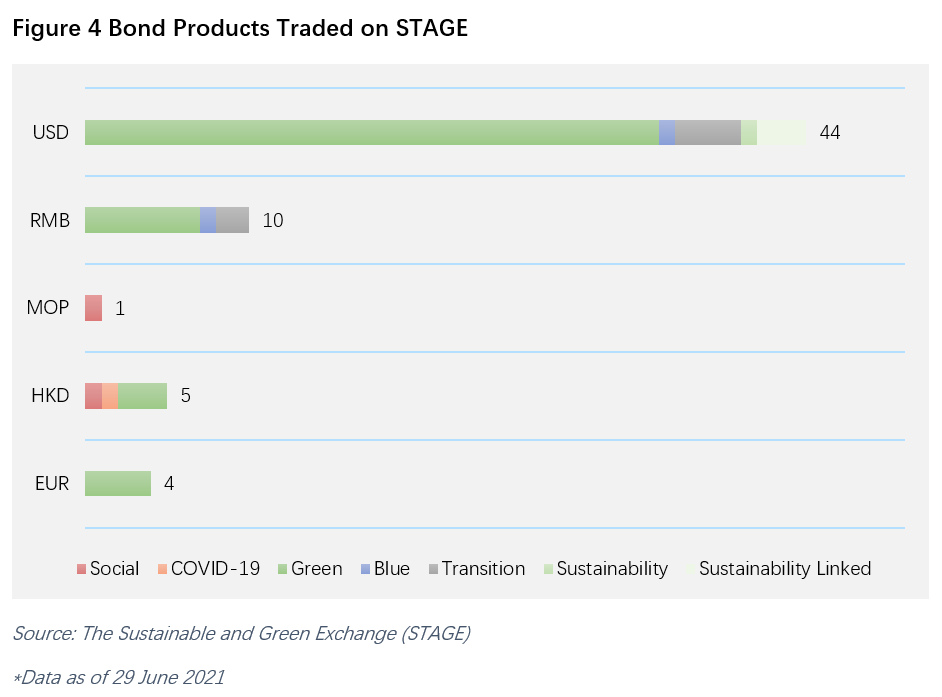

The HKEX officially released its Sustainable and Green Exchange (STAGE) in December 2020 as an attempt to boost Asia’s presence in the global green finance market, and more essentially, to unlock the potential of sustainable finance in the Greater China region.

By June 2021, STAGE offered up to 64 bond products, which are categorized into sustainability, sustainability linked, green, social, transition, blue, and COVID-19. Of these, 14 bond products were issued by Bank of China. Green bonds were the most-issued type of products with 49 green bond products outstanding, followed by 6 in the transition bond category. Notably, 44 of the 64 bond products are denominated in USD, followed by 10 in RMB and 5 in HKD.

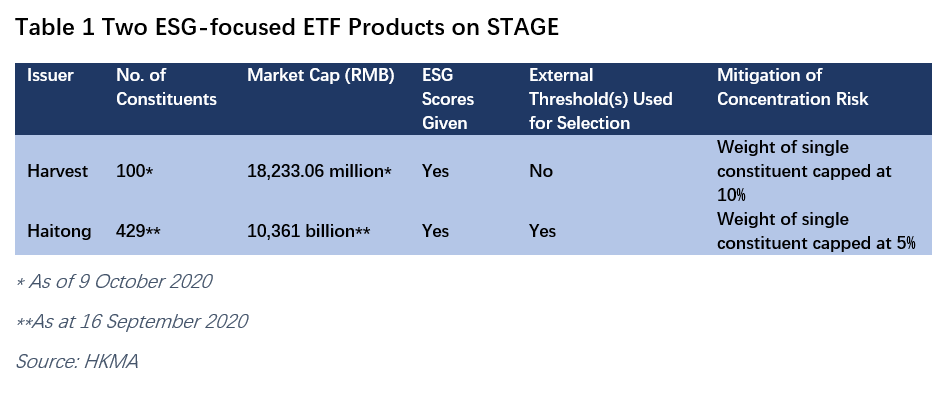

Three Exchange Traded Fund (ETF) products are also available on STAGE; two that focus on ESG issued by Harvest Global Investments Limited and Haitong International Asset Management (HK) Limited, and one which covers clean energy by Mirae Asset Global Investments (Hong Kong) Limited.