In recent months, electric vehicle (EV) prices in the China market rose rapidly.

In March, nearly 20 electric vehicle (EV) manufacturers announced price increases, according to our research. Leading EV companies, such as Tesla, BYD, XPeng and Li Auto raised prices for a number of models. The leading EV company NIO held out on price increases until April 11 when it announced that it would lift the prices of its ES8, ES6, and EC6 models by Rmb 10,000 starting May 10.

Tesla is the most sought-after EV brand by Chinese consumers. On March 17th, Tesla’s official website showed that the Model Y Rear-Wheel Drive, the company’s most popular model in China, rose by 13% from December 2021 to March 2022, an increase of Rmb 36,000.

Table 1 Price adjustments of leading EV companies since 2022

EV manufacturers pointed to the rising cost of lithium-ion batteries as the main cause of the price increases. Li Auto CEO Li Xiang wrote on his social media account, "Battery costs rose by an outrageous amount at the beginning of Q2 2021." The root cause is the unprecedented price spike of lithium and lithium salts, the most important components in EV batteries. CATL, the global leader in lithium-ion battery development and manufacturing, also announced that the company raised the price of battery products due to the spike in raw materials prices.

This is not the first time that the EV supply chain has felt pressure from rising material costs. Since 2021, rapidly rising EV sales contributed to supply shortages in both the upstream and midstream parts of the supply chain.

The market for Lithium hexafluorophosphate (LiPF6) is an excellent example of supply and demand imbalance. In 2021, this highly necessary stabilizing chemical component in battery electrolyte saw a rapid increase in demand from battery manufacturers. LiPF6 suppliers had difficulty ramping up additional LiPF6 production capacity, leading to a gap between supply and demand.

LiPF6 makes up 50% electrolyte raw material costs, or one of four main components of lithium-ion batteries. (Other three being cathodes, anodes, and diaphragms). Electrolyte price then directly led to higher end lithium-ion battery prices.

Prior to the run-up in LiPF6 costs, the manufacturing cost of electrolytes was approximately Rmb 25/kWh, accounting for about 4% of the total material cost of lithium iron phosphate (LFP) batteries and 6% of the material cost for lithium nickel cobalt manganese (NMC) batteries.

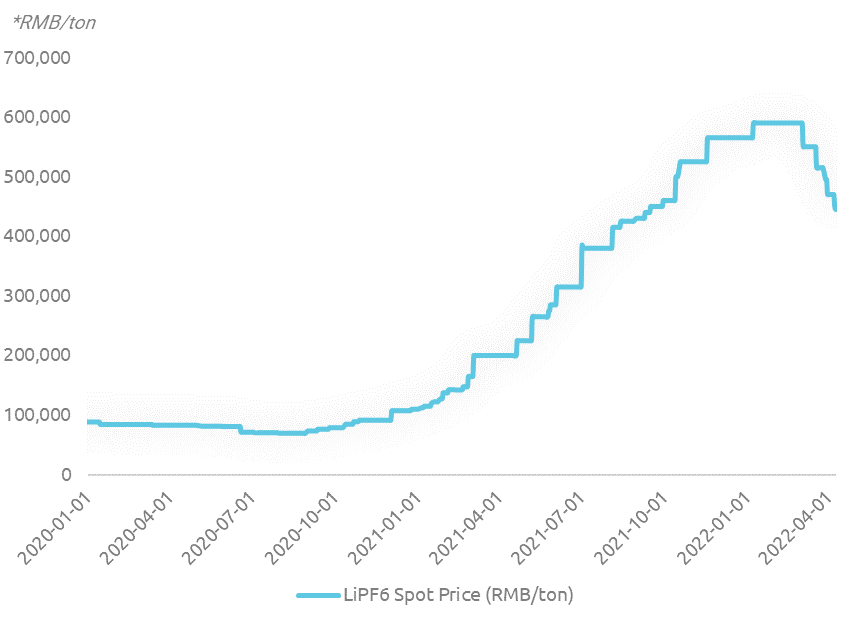

In early July 2020, the spot price of LiPF6 was approximately Rmb 70,000 per ton, according to Wind. By early 2021, the spot price rose to Rmb 112,500 per ton, and by year-end, soared to Rmb 565,000 per ton. In just one year, the market witnessed a fivefold price increase of LiPF6, a fine chemical product that was previously not in high demand.

Figure 1 LiPF6 spot price (2020 – present)

The Lithium Supply Situation

The current lithium price cycle began in Q4 2020, when the spot price of battery-grade lithium carbonate (i.e. Lithium carbonate with purity above 99.5%) was Rmb 44,000 per ton, the lowest quote in the prior four years.

Lithium carbonate, a type of lithium salt or lithium derivative, is a component extracted and refined from Spodumene (a lithium-bearing mineral) or mineral-rich brine. By early 2021, the spot price for lithium carbonate rose steadily to Rmb 58,000 per ton. Starting from Q1 2021, the spot price rose rapidly, followed by a plateau in Q2, and further rapid increases in Q3 and Q4, reaching Rmb 282,000 per ton by the end of December 2021.

After nearly a 5X increase through end-2021, price growth continued in Q1 2022 at an accelerated pace. As of 27 March 2022, the spot price of battery-grade lithium carbonate reached Rmb 500,000 per ton. Upstream Spodumene concentrate (5-7% Li2O) prices have also rebounded from their trough, with spot prices climbing from less than $400/ton to $2,050/ton, an increase of more than 400%.

Battery makers are experiencing major cost control challenges with the rising price of Spodumene concentrate and lithium salt. Based on the spot price and the reported EV battery direct material cost of Rmb 550/kWh disclosed by CATL in its 2020 financial report, at the beginning of 2021, lithium salt accounts for more than 6% of the total material cost in EV batteries. If calculated based on the spot price of Rmb 500,000 per ton, the cost of lithium salt alone is close to 300 yuan/kWh, accounting for 36% of the EV battery’s material cost.

Figure 2 battery-grade Lithium carbonate spot price (2021 – present)

Despite the lithium salt price spike, the EV battery supply chain did not collapse. We believe the following factors in long-term prices and weighed in:

- Manufacturers and traders of cathode materials experienced a sharp fall in inventory, according to numerous corporate announcements. With a supply shortage and no inventory to release onto the market, prices surged amid strong demand.

- Large EV battery manufacturers often purchase lithium salts on long-term contracts with upstream companies. The long-term contract price is at a substantial discount to the spot price. This helps reduce the immediate cost pressure of battery manufacturers.

- The supply-demand balance of other upstream raw materials for EV vehicles is also a fluid situation. For example, LiPF6 prices started to fall because of rising production capacity, reversing the supply deficit. This is starting to improve downstream profits and increase upside potential.

- EV vehicle manufacturers collectively raised retail prices, passing on incremental costs to consumers.

With the current round of material price increases driving up EV prices, we expect to see this affect marginal demand for EVs. Therefore, we expect the price of lithium salts to enter a period of greater stability in the next few months.

Revisiting the value of lithium resources

The reasons for sustained price increases in lithium resources are all related to mismatches between supply and demand. On the demand side, the EV market is growing at a compound annual demand growth rate (CAGR) of 40%-50%. On the supply side, lithium resource materials are in short supply due to insufficient capital expenditure in manufacturing capacity, coupled with long resource development cycles.

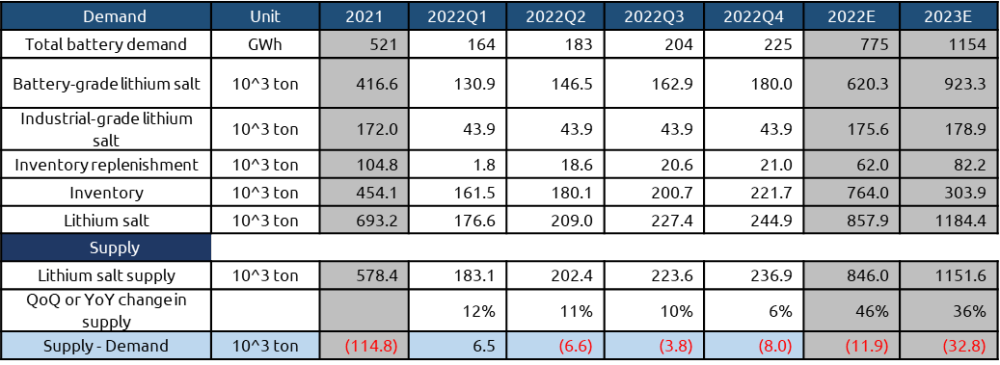

Table 2 Lithium salt supply and demand balance table

During the downward period of lithium prices in 2018-2020, the net profits of lithium miners contracted significantly. Lower profits have forced miners to reduce capital expenditures. For example, in August 2019, Albemarle (ALB US) announced plans to cut capital expenditures by $1.5 billion over the next five years due to plummeting lithium prices. However, the construction schedule of mining projects is relatively rigid, making it difficult to accelerate construction in the event of a rebound in profits..

The trough period of industry downturn will not only lead to delays in adding production capacity, but also increases the risk of mine closures. In the 2018-2020 lithium down-cycle, Western Australia's Wodgina mine went into production in April 2017 and ceased production in November 2019. The Altura mine went into production in March 2019 and ceased production in October 2020, right before the market showed signs of recovery. The Alita mine was the most unfortunate, as it started production in March 2018 and quickly went bankrupt in October 2019. The company has still not completed its bankruptcy-related restructuring, and the road to resumed production remains unclear.

The long development cycle also further limits the speed at which production capacity can be ramped up. On average, it takes about 15-17 years from the first discovery of a mine to reaching full operation. This roughly includes three phases: exploration and research stage, approval and licensing, and mine construction. On average, the preliminary exploration stage takes the longest, and the time required for this stage is strongly influenced by the company’s own decisions. The progress of this stage can be significantly accelerated during an industry boom cycle. As the project advances to later stages, the approval and construction periods are relatively rigid, leaving little room to speed up development.

We have identified a list of lithium mines that are likely to be put into production in the next two years, including: the expansion of Greenbushes mine of Albemarle (ALB US) and Tianqi Lithium Holdings (002466.SZ), the resumption of production of Wodgina mine of Mineral Resources (MIN.AX) and Albemarle (ALB US) and Ngungaju mine (formerly Altura) controlled by Pilbara (PLS.AX). AVZ Minerals’ (AVZ.AX)-invested Manono mine is likely to see the most significant addition in 2023.

Midstream and downstream enterprises in the supply chain have also seen that lithium salt has become a new supply bottleneck. These companies are looking to adjust their upstream suppliers. As early as 2021, CATL (300750.SZ) and Ganfeng Lithium (002460.SZ) staged a battle for the acquisition of Vancouver-based Millennium Lithium, attracting widespread attention in the industry. In recent months, CATL successively established subsidiaries in Ganzi Prefecture, Sichuan, and Yichun City, Jiangxi, to cooperate with local mining companies and state-owned enterprises to promote the exploration and development of lithium mines. Gotion Hi-Tech (002074.SZ), another major lithium-ion battery manufacturer, invested in the construction of a battery-grade lithium carbonate project with an annual capacity of 50,000 tons in Yichun City, Jiangxi Province, which is scheduled to be completed in Q4 2022. In addition to its deep ties with Youngy Co., Ltd. (002192.SZ), which owns rich Spodumene reserves in Sichuan Province, BYD (002594.SZ) recently invested Rmb 3 billion in Chengxin Lithium (002240.SZ). The latter currently has a lithium salt production capacity of 70,000 tons/year. After this investment, BYD's stake in Chengxin Lithium is expected to exceed 5%, further increasing its lithium resource supply reserves.

The Valuation Myth

In 2021, lithium mining companies were sought after by the Chinese capital market. Tianqi Lithium (002466.SZ), Ganfeng Lithium (002460.SZ) and Youngy Co. Ltd. (002192.SZ) showed respective increases of 172%, 41% and 217% for the year. Young Co., Ltd., owner of the largest lithium mine in China, the Jiajika mine, rose 458% at one point during the year. However, since Q4 2021, their share price has underperformed. As of the close of March 28, Ganfeng Lithium's share price nearly halved from its peak, with a drop of 45%. Tianqi Lithium and Youngy have also dipped by 43% and 38%.

Companies in the EV supply chain, such as battery cathode material manufacturers Ronbay New Energy (688005.SH), Beijing Easpring (300073.SZ), Shenzhen Dynanonic (300769.SZ) have benefitted from rising lithium prices over the past year as they can enjoy higher valuations than mining companies. The same can be said for lithium-ion battery producers such as CATL (300750.SZ), Gotion Hi-Tech (002074.SZ), and EVE Energy (300014.SZ)

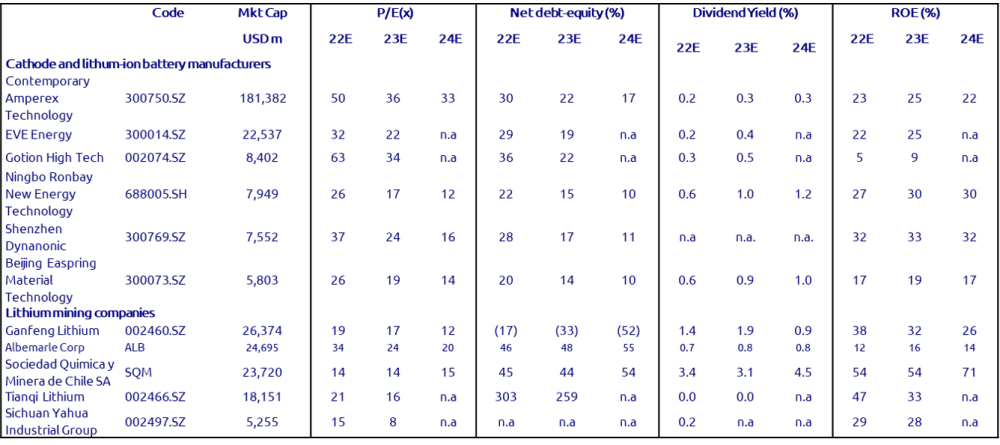

Table 3 Valuation table of selected cathode material, lithium-ion battery and lithium mining companies

On the demand side, we believe that through 2025, demand for new energy vehicles will maintain a compound annual growth rate (CAGR) of more than 40%. For the other major demand source, electrochemical energy storage systems, we expect the annual compound growth rate of demand for lithium-ion batteries to reach 50%. On the supply side, the investment and expansion of lithium mining capabilities (including ores, salt lakes and mica) face a number of constraints.

Another view in the market is that the government will use administrative measures to intervene in lithium salt prices. On March 16, the Central Government’s Ministry of Industry and Information Technology (MIIT) gathered lithium mining enterprises, lithium-ion battery manufacturers, and EV manufacturers to jointly hold a symposium. Reportedly, the theme was to promote “reasonable and stable” lithium prices, with particular emphasis on mining enterprises to collaboratively promote the sustainable development of the industry. However, it is also worth noting that China currently only accounts for about 20% of the world's lithium supply (Australia and Chile are the two major suppliers), but refining capacity and EV manufacturing capacity account for nearly 50% of the world's total, which implies that China still does not have strong pricing power for lithium.

Cathode materials and lithium-ion batteries are both China’s core assets in the climate tech industry, and the Chinese capital market has given these companies a considerable valuation premium. But without a secure supply of lithium, these assets are exposed to significant supply chain risk. At the same time, this round of price hikes reveals the importance and growth potential of the lithium mining industry in the EV value chain. The lithium mining industry may be undervalued in the era of global electrification and decarbonization.

Reference Links:

1. https://irm.cninfo.com.cn/ircs/question/questionDetail?questionId=1003627144572850176

2. https://www.catl.com/uploads/1/file/public/202104/20210430094928_4n1av8qek4.pdf

3. https://www.100ppi.com/vane/detail-.h1162tml