The US Securities and Exchange Commission proposed its first ever climate-related disclosure rules of 500+ pages on March 21, aiming to enhance and standardize climate-related information to address investor needs.

The SEC is proposing all listed companies to disclose their Scope 1 and Scope 2 emission data, to be filed along with registration and period reports such as the 10K. Should the proposal pass as scheduled December of this year (2022), listed companies would be required to start reporting on financial years starting in 2023 or 2024 depending on their market cap size.

The GHG Protocol’s emissions classification is as follows:

- Scope 1 emissions: direct GHG emissions that occur from sources owned or controlled by the company. These might include emissions from company-owned or controlled machinery or vehicles, or methane emissions from petroleum operations.

- Scope 2 emissions: indirect emissions primarily resulting from the generation of electricity purchased and consumed by the company. Because these emissions derive from the activities of another party (the power provider), they are considered indirect emissions.

- Scope 3 emissions: indirect emissions not accounted for in scope 2 emissions - generated from emissions from sources that are not owned or controlled by the company, e.g., the production and transportation of goods a company purchases from third parties, employee commuting or business travel, and the processing or use of the company’s products by third parties.

What to disclose:

- The listed company would be required to disclose Scope 1 and 2 in discrete and aggregate data but not including carbon offsets (such as how much emission in GHG types such as carbon dioxide, methane, etc) as well as intensity (how much emission per unit of economic value or production).

- Scope 3 emissions if they are material or if the registrant has set a GHG emissions reduction target or goal that includes Scope 3 emissions. Smaller reporting companies, or SRC’s, are exempted from Scope 3 emissions reporting.

- Information regarding the oversight and governance of climate-related risks by board and management.

- Climate-related risks with material impact on business and financial statements that would manifest over the short-, medium-, or long-term, as well as climate-related events (such as severe weather etc.) and transition activities with impacts on the line items of financial statements.

- Climate-related risks - processes for identifying, assessing and managing risks and integrating into the risk management process.

- If the listed company has publicly set climate-related goals and targets, information about the scope, relevant data to indicate whether progress is made, and amount of carbon offsets or renewable energy certificates (RECs) if used.

Source: What Scope 1, 2 and 3 emissions involve. Chester Hawkin/Center for American Progress, MioTech

Who and when to disclose?

SEC’s proposal distinguished different registrants and filers depending on their float size.

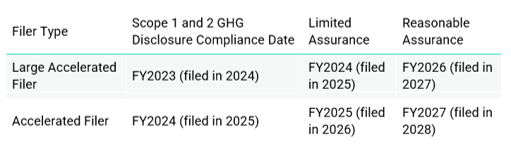

- A large accelerated filer is an issuer with an aggregate worldwide market value of US$700m or more.

- An accelerated filer is an issuer with an aggregate worldwide market value of USD75m or more, but less than US$700m.

- A Small Reporting Company is a company that has public float of less than $250 million or it has less than $100 million in annual revenues and no public float or public float of less than $700 million.

Table: Disclosure compliance date by registrant type

Table: Assurance requirement by filer type

- Building on existing frameworks The proposed requirements are like what many companies already provide for other accepted disclosure frameworks such as Task Force on Climate-Related Financial Disclosures (TCFD).

We find that larger companies have been more likely to comply with disclosure recommendations. The 2021 TCFD Status Report reviewed the disclosures of 1,651 public companies and revealed that 26% of the companies with less than USD3.5b in market cap disclosed scope 1, 2, 3 GHG emissions in 2020, and only 12% of them disclosed board oversight of climate risks. - Regulation net is spread wide to most companies The current SEC proposal for disclosure is much more comprehensive and will affect more companies than the existing recommended disclosure frameworks. More mid-sized US-listed companies will need to take actions to measure and report their climate-related information in the coming year, especially those with a market value over USD700m.

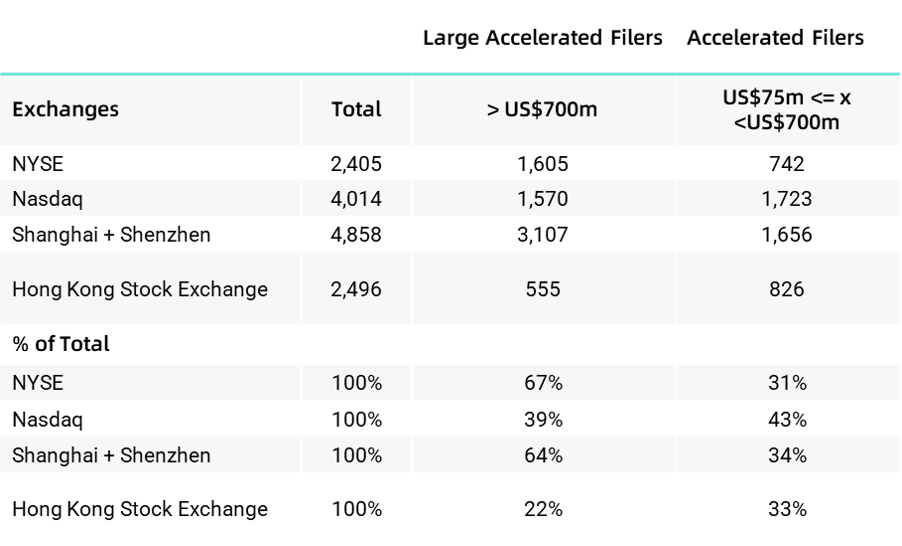

Based on current data the end of 2021, we find that almost all (98%) of the listed companies on NYSE would be counted as a Large Accelerated Filers or Accelerated Filers (with market value above US$75m). A total of 3,293 companies, or 82% of the total companies listed on Nasdaq would be count as such and be required to disclose Scope 1 and 2 emissions by 2023 and Scope 3 emissions by 2024.

If the same SEC disclosure requirement were to apply to the A-share companies in China, the proportion of the companies that would be affected would be very similar to that of NYSE, with 64% of the companies with market cap over US$700m and regarded as Large Accelerated Filers and 34% as Accelerated Filers. Hong Kong exchange has a higher concentration of smaller cap companies. Those with market cap under US$75m accounts for almost half (45%) of the entire listed companies.

- The North America region lags Europe in overall TCFD-aligned disclosures with 42% of the reviewed companies making disclosures on average across different topics. In the research by Financial Stability Board (FSB), a total of 21% of the North American companies that were reviewed disclosed scope 1, 2, 3 GHG emissions compared to 64% in Europe, 42% in Asia Pacific, 26% in Middle East and Africa, and 25% in Latin America.[4]

According to the Science Based Targets initiative (SBTi), 401 US companies have set a climate target, which include the big names like Walmart, General Motors, and Microsoft, while only two companies’ targets cover scope 3 emissions, JLL and CVS Health. This echoes Reuters’ finding from S&P Global data that although 35% of North American companies have set greenhouse gas targets, those plans do not include scope 3 emissions [2]. A total of 125 US companies has a net-zero commitment.

Figure: Companies with climate targets in United States

- Affecting Chinese ADR’s. As the SEC proposal will apply to both domestic and foreign private issuers, with draft proposal encompassing foreign companies listed in the US, such as the 200+ Chinese ADRs. However, we believe climate disclosures would not likely be the driving reason for Chinese companies to delist from the US exchanges, as re-listing in Hong Kong would mean the similar TCFD-recommended framework starting from 2025.

Delisting would continue from the previous SEC rule in June 2021 that would suspend companies from trading starting 2024 if they fail to provide sufficient disclosure and access to US-approved auditors, furnishing audits for three consecutive years. Beijing bars from foreign inspection of working papers from local accounting firms. - Helps with long-term pollution reduction goal President Biden set the target to reduce US greenhouse gas pollution by 50-52% by 2030 compared to 2005 levels. The disclosure requirement is an important step toward keeping investors and corporates accountable toward the long-term goal.

- Opposition expected We would expect opposition from some Republicans in Congress and the US's Chamber of Commerce. The Chamber said that the rules would force companies to disclose largely immaterial information at the price of more meaningful data [2]. However, in the draft proposal, the SEC notes that it has broad authority to promulgate disclosure requirements that are “necessary or appropriate in the public interest or for the protection of investors” under the Securities Act. The public will have 60 days to submit comments and the final rule will be voted on by SEC’s four commissioners, a process of a few months.

- Adding compliance, litigation and technical information infrastructure cost Companies will need to add to their compliance capability to prepare the right disclosures alongside the annual financial statements. Legal department will need to be prepared for the possible resulting litigation that are expected with the added transparency and reconcile with previous set targets and goals and risk management in place. Technical capabilities in accurately tracking carbon footprint would also be expected as a result of the SEC climate disclosure proposal.