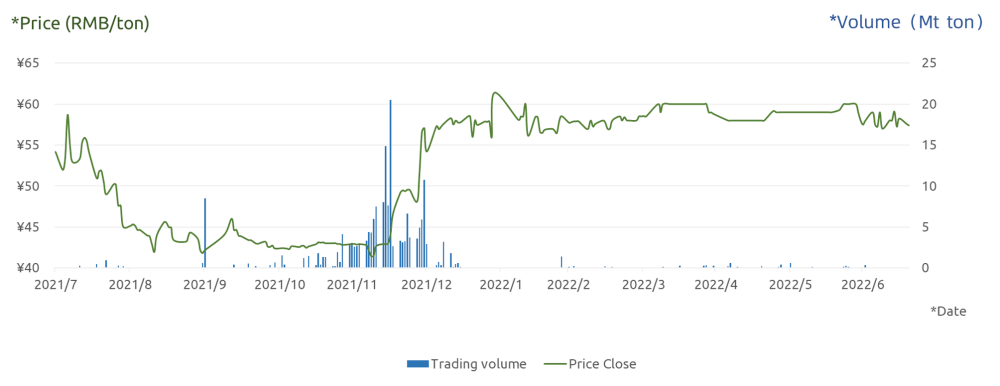

China’s national emission trading scheme (ETS) celebrated its one year anniversary on July 16, 2022 with 52 weeks and 242 trading days and a cumulative volume of 194 million tons of China Emissions allowances (CEA) traded and a cumulative turnover of RMB 8.49 billion (US$ 1.26bn). More than 2,000 power companies nationwide participated in the national ETS trading market and completed the first compliance period, with a compliance rate of 99.5% based on compliance volume[1].

Chart: National ETS daily close price (RMB/ton) and trading volume (Mn ton)

At the beginning of its launch, the Ministry of Ecology and Environment had high hopes for the national ETS. “The national ETS is a major institutional innovation to use market mechanisms to control and reduce greenhouse gas emissions and promote green and low-carbon development...In the next step, the market will gradually expand its coverage to more high-emission industries, enrich trading varieties and trading methods as needed, achieve smooth and effective operation. This will enable the market mechanism to play an effective role in controlling greenhouse gas emissions and achieving China's carbon peak and carbon neutrality targets.”

There has been much initial emphasis on the market mechanism of the carbon market, or the price discovery function as the core value of the national ETS. The inclusion of more industries, the enrichment of trading varieties and methods, and the assurance of achieving the market effectiveness are the focus of the regulators for the coming years.

However, the successful completion of the first compliance cycle has been accompanied by concerns of the characteristics of the compliance-based ETS and the lack of market liquidity. Let's take a closer look.

Power generation sector first pioneer in national ETS

Currently, the national ETS includes only the power generation sector, which emits approximately 4.5 billion tons of greenhouse gases annually, accounting for nearly half of the country's total carbon emissions (10.5 billion tons[2]). The power generation sector is mainly composed of SOEs, and the power generation processes of fossil-fueled power plants are similar, making the accounting of their carbon emissions relatively intuitive. However, the feedback from the end of the first compliance cycle shows that there are still plenty of problems with the power generation industry alone, which are concentrated on the poor quality of carbon verification data (described later in detail).

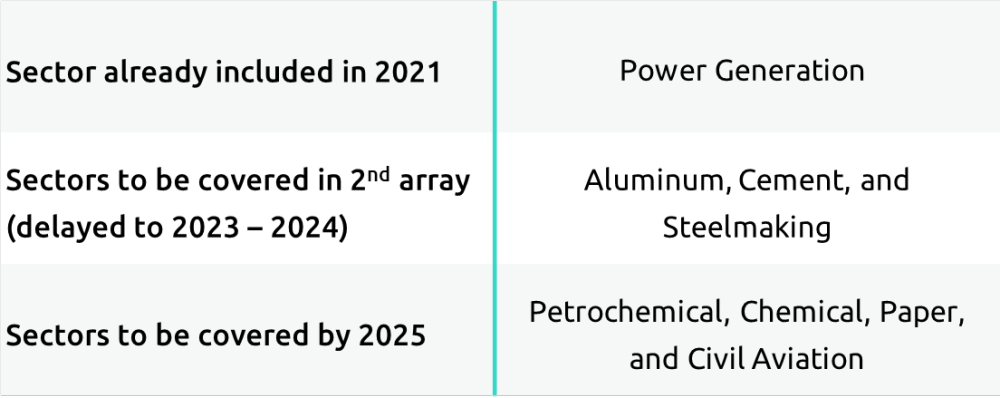

The steel, aluminum and cement sectors, which were previously highly anticipated to be included in the national ETS by the end of 2022, still have not received relevant policy signal yet, thereby it can be presumed that the inclusion will be delayed until at least 2023. It also means that during the second compliance cycle of the national carbon market (2021-2023, the current compliance cycle of the national carbon market is 2 years instead of 1 year), still only power companies are subject to the national ETS emission allowances. In the earliest plan, in addition to the above three sectors, the petrochemical, chemical, paper and civil aviation sectors will be included in the national carbon market during the 14th Five-Year Plan period.

Table: The sector coverage of the national ETS during the 14th Five-Year Plan period

Instruments and trading mechanisms

The traded instrument in the national ETS is China Emissions Allowance (CEA), or spot carbon allowances. In terms of trading mechanism, it allows for listing trading in the exchange as well as OTC block trading.

Take the EU ETS for instance, European Union Allowance (EUA) and Aviation Allowance (EUAA) are the counterpart to the CEA in China’s national ETS as the main spot instruments. The difference is that EU ETS introduced various derivative instruments from the very beginning of its establishment, including EUA futures, options, swaps, etc. Among them, EUA futures are the most popular derivative with important price discovery and risk hedging functions. EUA futures are also much more actively traded relative to spot, accounting for over 90% of all EUA traded volume[3].

The OTC block trading accounts for 161 million tons of spot CEA traded volume, or 88% of the total volume, while the exchange-listed trading occupies 12%. The huge difference between the two indicates that emission enterprises are less willing to deal CEAs with the exchange listing, which results in an inactive and illiquid spot listing transaction system. This lack of liquidity has a few implications. Firstly, for companies with trading needs (e.g., those with surplus allowances or those that need to purchase additional allowances for compliance), there will be a considerable liquidity premium/discount for large transactions on the market. Also, the questioning effectiveness of allowance price signal makes it difficult to guide enterprises' emission reduction strategies and decisions.

The problematic carbon footprint verification

The cornerstone of the effective operation of an ETS is the accuracy, authenticity, and validity of carbon footprint verification data, which is guaranteed by the MRV mechanism, or monitoring, reporting and verification (MRV). China’s MRV mechanism takes the sector-based approach - a separate GHG emission accounting method guide is applied for each covered sector. Since 2013, several organizations have jointly prepared pilot versions of the guides for a total of 24 industries.

Among them, power generation has been one of the sectors with better basic data and easier accounting. Along with the kickstart of the national ETS, power generation sector is also the first to be issued the Corporate GHG Emissions Accounting Methodology and Reporting Guide for Power Generation Facilities (Revised Edition 2021). Feedback from the first compliance period however shows that the quality of carbon footprint verification data is still worrying. In a briefing by the Ministry of Ecology and Environment in March this year, four agencies were exposed for tampering with and falsifying test reports, producing false coal samples, and distorting and misrepresenting report conclusions, among other outstanding issues.

The briefing did not disclose the penalty results, however. According to the Carbon Emission Trading Management Measures (Trial) issued by the Ministry, the maximum fine that can be imposed on the emission control enterprises is RMB 30,000 and the penalty for third-party verification agencies was not stated. The rather affordable potential maximum penalty of RMB 30,000 makes falsification more enticing. One data entry slightly twisted by a carbon verification agency may grant the enterprise millions of tons of emission allowances, which then translates to millions of dollars for the company profit.

In response to the exposed carbon emission data quality problems, the new Corporate GHG Emissions Accounting Methodology and Reporting Guide for Power Generation Facilities (Revised Edition 2022) has been revised to strengthen the process management of carbon emission data and refine the quality control requirements for accounting and reporting.

While improving data quality issues in carbon emission from the power sector is currently on the agenda, so is the introduction of accounting methodologies and guidelines for the remaining seven sectors. They could be more difficult to account for than the power sector; the chemical industry for example, could emit as many as seven types of greenhouse gas emissions. The more types of raw materials and processes in other industries would add more complexities in calculating carbon emission levels.

Although the timeline for adding the remaining sectors has been delayed, the authorities should be preparing for an update and revision of the GHG accounting methods for the cement, aluminum, and steel industries.

Breaking through the challenges

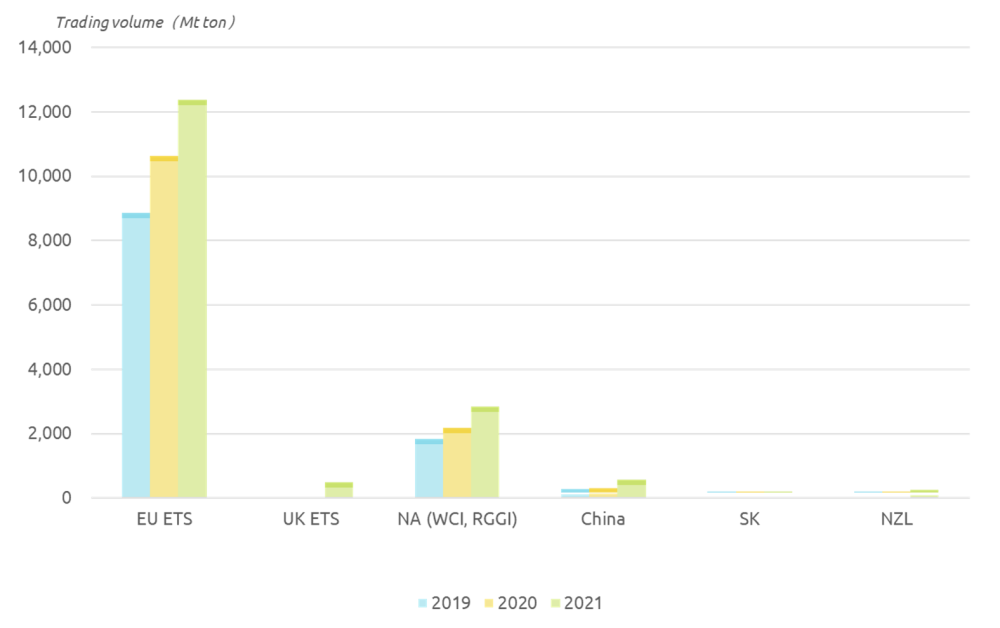

As a market-based measure to promote emission reduction, emission trading scheme is an important policy tool to reduce the comprehensive cost of emission reduction for the whole society. ETS plays an important role in promoting energy restructuring and resource allocation optimization. Historically, other carbon markets around the world also have had slow starts at the beginning of their launches. For example, in 2005, the first year of the EU ETS, a total of 321 million tons of allowances were traded. By 2021, this figure reached 12 billion tons.

Chart: Historical trade volume of major carbon markets (in millions of tons)

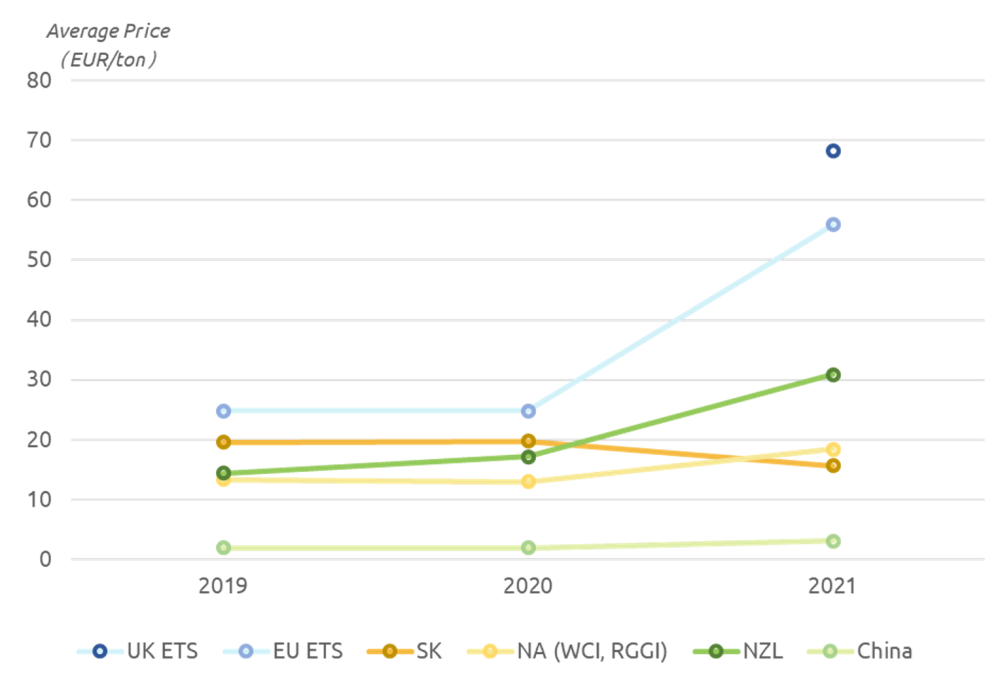

Chart: Average trading prices in major carbon markets, 2019-2021 (in EUR)

However, the macro environment of global climate politics has put new external pressure on the development of China’s national ETS. The price of the EU allowance has now reached EUR 83 per ton, which is more than 10 times the CEA price. In addition, the EU carbon border adjustment mechanism (CBAM) is likely to be approved at the end of this year and to take effect in 2027. The CBAM is expected to levy carbon tariffs based on the difference between the EU carbon price and the importing country’s carbon price, exposing risks to China's foreign trade relating to the current low explicit carbon price in the national ETS. Building a carbon market that enables price discovery and demonstrates China's contribution to carbon reduction is particularly important today.

Moving forward – the evolving carbon market

We expect that the increase in the number of participants and the introduction of new trading instruments will bring much needed liquidity to the currently under-active carbon market. Currently, financial institutions and speculators are not allowed to participate in the national ETS. Financial institutions could participate in the carbon market as market makers or asset owners, thus creating a different kind of trading behavior from that of emission companies, which will increase the market activity and strengthen the price signaling mechanism. By then, emission allowances could become a new asset class and financial institutions could introduce more diverse products to the market. For example, in March this year, CICC launched the first carbon futures ETF CICC Carbon Futures ETF (03060.HK) on the Hong Kong Stock Exchange. The ETF tracks the ICE EUA Carbon Futures Index which measures the performance of a long-only basket of ICE EUA Futures Contracts.

Another means to increase liquidity in the carbon market is the introduction of derivatives. Besides, derivatives such as allowance futures and options could also enable emission companies to trade allowances in a more cost-efficient manner, as well as manage their positions on carbon exposure. Derivatives markets also play an important role in improving transparency by providing forward-looking price signals on carbon prices, which can help achieve long-term sustainability goals and provide regulators with useful signals on carbon price regulation.